This Moment in Art History

I’ve been thinking a lot about art since the wealthy started staging their 1% putsch. It’s no real exaggeration to say AI is a tool of attack on the creative class by dull rich dopes unsatisfied with ownership and angling for dominion. Visual art in particular is unique among the arts as a sort of singular performance.

My feeling is that the rich both hate and respect art because it’s the one human creation that defies their attempts to game/control it. They often lack an ability to appreciate it on an aesthetic level, but they can at least possess it.

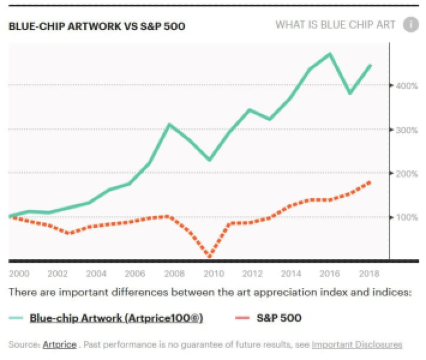

However the process demands they surrender to a consensual reality of value unlike most investments, where worth is entirely subjective. Almost as an extension, there isn’t a reliable secondary market. Even more than stocks, it’s something you have to hold for decades for it to fully appreciate.

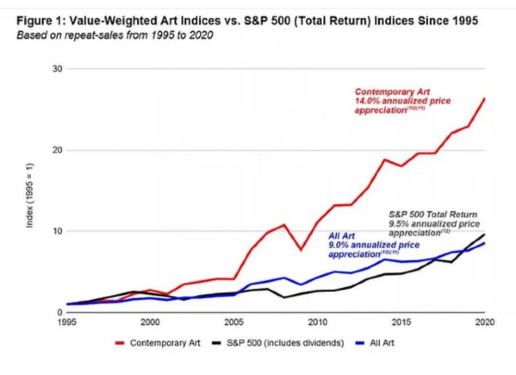

The average hold rate of resold work last year was 27 years, up from nearly 23 in 2024, with work resold within five years losing almost 10% of its value, and works held for more than two decades posting annualized yearly returns of 9.6%. This consistency – if you choose well – is its appeal for the rich: According to Artprice, “blue-chip” art posted annual returns of 8.9% from 2000 to 2019. (S&P 500 returns were 6%-7% in that period.)

This gives the wealthy an unusual vested interest in art, museums and cultivating a popular interest in it, that their portfolio might realize a better return over time, even as the rest of us hope to realize a more instantaneous “profit” viewing it. Rarely are class incentives this closely intertwined!

I did some visual arts writing/critiques in my twenties, and like many have always loved art. My house is dotted with prints, with some in storage that are recycled back in periodically, much like a gallery, as the pique fits. As the residential environs has grown more homogenized over the decades, I’ve compensated by making my home more eclectic, artistic and odd. When I travel, the area museums are atop my list of places to visit.

Similarly there has been a global societal push to make art more accessible to the masses, with many museums waiving admission fees. (They’ve discovered greater foot traffic compensates with more gift shop purchases, which constitute as much as 40% of museum revenue, improving – without fully covering – lost ticket revenue.) This began in part with pop artists like Warhol and Haring. It seems to have seeded a more approachable vibe overall. (Orchestras seem to have also taken the cue.)

It contributes to my curiosity about this growing scene, particularly in how it directly varies from music artists for reasons that go back to the Medicis, and the way art is valued, which I hope to explain while surveying how the art scene has changed in the past three decades and where it’s at this moment. Not for any particular reason, but just because.

Is it a Boom or a Bubble

The scene has been subject of a raft of boom/bust articles for the past decade at least, as people obsess over what seems to be simple variability.

Art investment is at its core a speculative market, even more than just about anything else in creation, because the unique nature of most works bestows a scarcity no mass medium can rival (with the arguable exception of Wu Tang’s 2007 single-pressed album, Once Upon a Time in Shaolin, which financial swindler Martin Shkreli briefly owned). Since a work is singular, it requires another buyer who shares similar “values”. (In this world. Imagine.)

Like anything else in the culture, some things have proved enduring than others. For a long-time a lot of the art scene’s value was tied up in the Grand Masters. In 2017, DaVinci’s Salvator Mundi sold for $450 million after a pitched competition lasting for 19 minutes in Rockefeller Center before over 1000 onlookers and participants, between buyers bidding on behalf of Saudi Arabia's Crown Prince Mohammed Bin Salman and Mohammed Bin Zayed of United Arab Emirates. The end came when the bid leapt from $330M to $400M! (That’s a cool $50M total in fees.)

Why this painting? Well it’s the last confirmed Da Vinci in private hands. It has previously been owned by King Louis XII of France, King Charles, King Charles II and King James II of England before vanishing for almost 200 years. It was discovered, a veritable wreck, hidden beneath overpaints, and long mistaken as a copy. It sold at Sotheby’s in 1958 for £45 then at a regional auction in the U.S. in 2005 for $1175, as it was assumed to be a copy or a follower.

(It took six years of authentication to prove otherwise; there are apparently 20 other lesser copies, but details, such as Christ’s hands and ringlets of hair suggest the handiwork of Da Vinci, which was never really in doubt. Some continue to argue it was done primarily by others in his workshop with Da Vinci providing key touches but x-ray analysis argues otherwise.)

Most of the biggest movers are time-honored masters.

Two Rembrandts sold for over $180M in the last decade, Standard Bearer, and the full length pendant portraits of Maerten Soolmans and Oopjen Coppit. Gauguin’s Nafea Faa Ipoipo? (When Will You Marry?) sold for $210M in 2015, Paul Cezanne’s The Card Players sold for $250M in 2011, and Gustave Klimt’s Portrait of Elisabeth Lederer sold for $236.7M last year, after his painting Water Serpents sold for $170M in 1970.

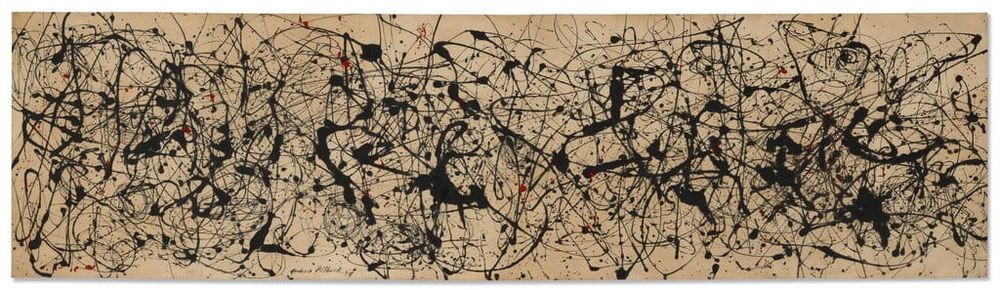

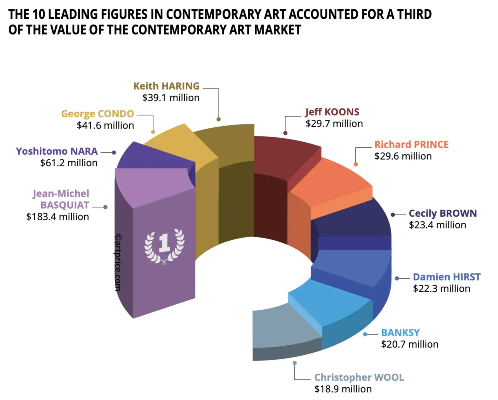

Of the more modern artists, a record four Picassos have sold for over $100M. Key abstract expressionists Mark Rothko, Jackson Pollock and Wllem de Kooning, and pop artists Andy Warhol also are among the dozen artists with paintings to sell for over $170M. In May, Pollock's 7A ($181M) sold at the same auction that Rothko's 1964 painting No. 15 (Two Greens and Red Stripe) sold for $98.4M with fees.

Obviously this is the high-end, and that's generally considered any painting that’s sold for over $10M. It’s a market entirely driven by supply. For example, the Kaplan family’s Leiden Collection has 17 original Da Vincis, rivaling the 22 held by the Rijksmuseum in Amsterdam.

Through the middle of last year, there was a lot of concern. The high-end had been in the doldrums since just after the pandemic. In 2024, the number of $10M+ work fell by 39%, and overall percentage of sales by such works shrunk from 23% in 2023 to 18% in 2024. Only three works “hammered” over $50M (without fees) after twice as many in 2023. The first half of last year seemed even grimmer. The global art market shrank by 16% from 2022 to 2024, and at the midway point last year sales were down another 8.8%.

Then several prime collections went to auction in November, from Estée Lauder heir Leonard Lauder, and Robert and Patricia Ross Weis of Weis markets, and Hyatt heirs, Jay and Cindy Pritzker, grandparents of Illinois governor, JB Pritzker. The Pollock in the title sold auction featuring 16 works from Si Newhouse's collection, which Christie's sold in the first part of the evening for $630M as part of a $1.1B night at the auction. The Pollock is one of the few of scale still in private hands.

That’s the thing about the high-end market – nobody is flipping them to make a profit. The only time such work becomes available is death, debt or divorce, known as “the 3 Ds.” This sudden influx of rare top shelf work including the $236M Klimt work, now the fourth-most expensive painting in the world, and the second-most expensive painting sold at auction after Salvatore Mundi, helped the year eke out a modest 4% gain.

It ended a bad streak for the art market, which fell off badly without auctions, galleries and art fairs to publicize work during the pandemic, then bounced back nicely in 18 months, quickly got frothy, and fell off the ensuing years.

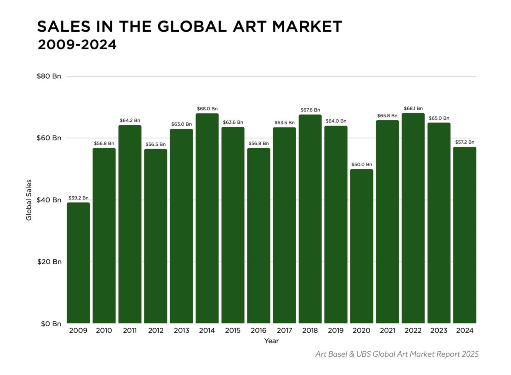

For all the talks of bubbles and busts, the art market has been remarkably stable for years, hovering around $60B globally. While that might sound like a lot, it’s dwarfed by the $300B luxury goods category annually, with brands like Hermes boasting valuations that high themselves.

Here’s a chart. While the industry grew quite fast after the millennium, it's mostly been in the $60M range ever since.

The industry essentially doubled in size from around $30M in 2002 to over $60M in 2007, before dropping to under $40M in 2009 after the financial crisis, then bouncing back. It’s pretty much held at $60B for the last two decades, with a remarkably steady ebb/flow of three-to-four year intervals.

Such talk of boom or bust seems to amount to little more than hype and despair in an arena where value builds slowly. Collectors and foundations get it. Not only is around half of high-net-worth collectors’ spending on works by new and emerging artists, getting them early in their career and purchasing works (70% of the time) within a year of completion. (This is also why it’s so hard for novice collectors to excel in the “buy low” field – it’s already crowded, wildly subjective, and expertise only goes so far!)

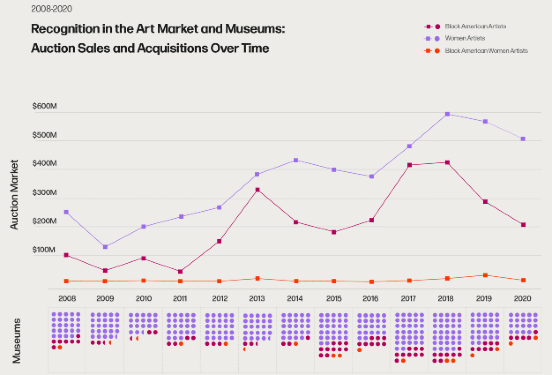

Suffice to say that there are several different layers of the art market. As a whole it’s speculative top-to-bottom, and the overall strategy is definitely “moneyball” (exploit market inefficiencies), like women artists or surrealists, both of whom saw large upswings recently, as tastes subtly migrate with the addition of new generation of collectors.

The Conundrum of Value & New Artists: Let’s Talk Patrons!

One of the allures of art collection is probably similar to the allure of art itself: Nobody can tell you what a great piece of art is, but if you know, you know, and people will pay for that knowledge in a world where such aesthetic consensus is achieved through a combination of luck, gamesmanship, timing and vision/talent. One has to be well-connected to be able to A Beautiful Mind those numbers.

The only people with enough context to know what’s actual fresh and have an inkling of what’s tired are generally gallery owners, who are essentially the agent/manager of a stable of artists with exclusive right to sell their work.

As you might imagine, the top galleries attract the top talent because they promise the biggest paydays, and for this reason, gallery owners have dramatic vested interests. Further, their status is predicated on their quality and throughput, attracting the kind of whale investors that subsidize the art world.

Now pause for a moment and try to think of any other business where the closest thing to experts on the worth of your investment are also the people trying to sell you their artists. Unaligned incentives, anyone?

Canice Prendergast, an economist at University of Chicago Booth School of Business, who runs the school’s contemporary art collection, has spent years exploring the vagaries of the scene. Like with stocks, the value of expert and inside opinion is such that the connected do far better than the amateurs.

“The well-connected get information earlier than the rest of us, and the uninformed pick up the scraps,” Prendergast notes, comparing them to equities. “While most purchases yield no returns, for the lucky few collectors, a tiny sliver of them lead to a major pay day.”

This sort of need to have rich clients to get good artists and good artists to get rich clients is why it’s typically been much harder for smaller upstart galleries. A facet of the gallery world is that a gallery will charge what they feel the art is worth, not necessarily what its market is. And why should they?

As a result, gallery purchases typically do much worse at auction among all the but highest tier of artists. This is also why galleries will almost never lower their prices, because the cost is essentially indicative of the tier of are the owner (believes, or wants the buyer to believe) they are in. To lower the price essentially becomes an indictment of everything on the walls, in this rubric.

Gallery sales aren't usually competitive – it's the impulse buy of the art world.

Auctions need two parties that want the same painting in order to run up big prices. (Many paintings never make the "reserve rate" and aren't sold, though it's a pretty consistent rate.) This happens because the supply of blue-chip painting is scarce, not liquid, forcing up prices for that limited supply. Further, auction sales are loaded with enough fees to fund a family of failsons.

The seller must pay a commission (5%-15%) and the buyer's fees are 26% on the first $600,000, 20% on portion between $600K and $6M, then 13.9% above that. So on a mid-market lot hammering at $200,000, the buyer may pay close to $250,000 while the seller nets $185,000 or less. The house captures the spread. Sales are relatively infrequent, but the auction houses make up for it on volumet.

The private sale is an interesting case because while a value may or may not be reported, there is no documentation. There's a small commission they seller pays or the buyer agrees to split. The lack of documentation of a price history can be advantageous down the road, for multiple purposes from sale, to donation to, relatedly, tax planning.

This is one of several aspects of the industry that have long favored big name artists and galleries at the expense of smaller, newer artists. A similar dynamic is at work with small collectors.

Larger collectors, such as the ones we mentioned early, buy early into multiple artists’ career. The difference in value of appreciating art is so great, a well researched plan compensates for the (cheap) misses.

Part of the plan is, interestingly, to game public perception. The collector host touring shows that showcase the artists' work, hopefully in the context of better known artists/work to build salience. They will also contribute artist pieces to museums, packaging a nice tax break up with an investment in their catalog. This also allows them to preserve high artistic valuations the more rigorous auction market never would!

This works in part because of the legacy bent of the market. Unlike the popular art forms of music and movies, the value of the work has less to do with the present reception to any particular piece than how it fits within the artist’s oeuvre. You’re essentially trying to buy up a bunch of rookie baseball cards – with their value predicated on their full size of a career that’s only visible in the dimmest way when you purchase.

That’s why in this very subjective market, investing in an artist is much like buying an equity stake – your return-on-investment is deeply incumbent on how things go for the next couple decades, and you’re gonna lose more than you win, but like the music industry, hitting once can pay for all the losers.

All’s Fair in Love and Art

This milieu of knowledge in the hands of the few, and everyone feeling around in the dark started to change around the turn of the century with the rapid growth of art fairs – huge destination experiences, open to the public, where everyone from the curious to the well-heeled can eyeball an enormous amount of art with the expectation of finding something that keenly matches their sensibilities.

The initial impulse came from cities with bubbling art scenes beyond the art capitals like New York, London, Paris and Berlin. That’s how Art Basel, which started in 1970, changed the scene with its extended fair in Miami. Art Cologne started in 1967, but the art fair scene only blossomed post-millennium. Freize in London started in 2003, a year after Art Basel in Miami. Frieze and Art Basel have since expended to new locales including Seoul, Hong Kong and Los Angeles.

Though firm numbers are unavailable, there were less than 50 art fairs in the early aughts, growing to 419 at its peak, the year before the pandemic. There were 345 art fairs in 2024.

The fairs are popular because they drew huge crowds of people to a city, lured by the possibility of seeing thousands of pieces of work in a weekend, even more than housed in most cities’ museums.For the artists and galleries showing it offers a huge "opportunity" audience of the people that weren't going to be walking into a downtown gallery, but would visit an event like this.

The jet-setting aspect also helps lure in celebrities and CEOs with only a passing interest in art, but enough pocket money to make anyone’s weekend.

It was enough of a sea change that numerous galleries shut down, unable to compete as post-Covid (see, WFH) inner-city foot traffic shrank precipitously and art fairs became a part of a growing “experiential consumption” zeitgeist. A 2014 report from the Age noted a 30%-40% drop in gallery sales.

Unfortunately none of this was better news for smaller galleries – at least not so far. The costs of attending an art fair are expensive – a booth is priced by the square foot. Nearly half the galleries reporting spending over $40,000 per fair, 20% report $70,000-$140,000m which often doesn’t even procure a plum position, and 6% spend in excess of that. Yet with more than 30% of global art sales coming at art fairs, galleries can’t just pass them up.

These costs put a further crimp on newer artists who can’t typically command the sums necessary to make it worthwhile for a gallery, which increasingly must favor more established artists that can secure consistently higher rates.

The cost competition among fairs and the galleries that attend has recently drive galleries to pull back, picking their fairs more strategically. Fairs for their part have narrowed their focus and specialized, leaning into local regional artists, and stylistic or thematic themes.

Counter-events around fairs have also become more prevalent to the point where renting a U-Haul and turning it into an ersatz gallery is not crazy-person-talk but an actual thing which other people are adapting. (Hard concept to copyright.)

This adventurous spirit demonstrates how readily galleries and artist are adapting to the changing marketplace. For years, it was all about galleries in big cities, now it’s art fairs around the world. But the simple fact is that everyone sort of needs each other for anyone to make any money, much more so than the music or movie business.

Contemporary Art FOMO Bubble Bust

There was a noteworthy boom/bust cycle recently in one quadrant of the scene, contemporary art, launched mainly by noobs trying to buy new art like the pros do, which only drove up the price on a lot of unproven artists of (still) questionable quality.

What I’ve explained so far about the market is the way it generally works - most people invest in established value.

But right after the pandemic, probably partly incepted by the more limited access to art fairs and auctions which can act as a mediating factor on what can only be described as “irrational exuberance,” the scene endured a two-three year period of FOMO, when a similar market mania to that which drives people to invest in anything AI gripped the scene.

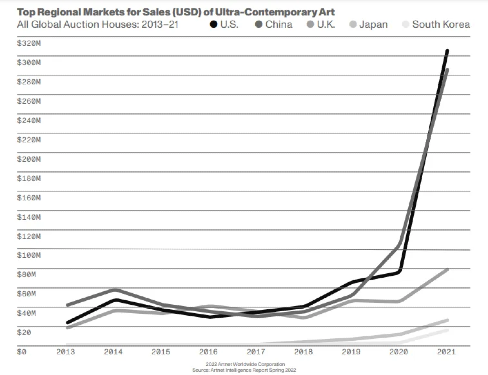

Collectors spent $712 million in 2021 on artists born after 1974 (known as the ultra-contemporary art market), nearly tripling the $259 million spent a year earlier. Like the dot-com feeding frenzy, a sense of scale was lost in the race for “easy money,” enriching everyone from meme-artist Alec Monopoly, to dead Canadian painter, Matthew Wong and multi-medium LA collagist/painter Jonas Wood, who in 2019 sold Japanese Garden 3 for $4.9 million.

Things were so flush, a market developed to quickly turn around these recently painted art, which was known as “Wet Ink.” While as noted earlier, the pro collectors are quite into buying art within a year of creation, so on the face of it, it’s not outrageous. But about 45% of the people buying art any year are doing it for the first time. It would probably not be an exaggeration to say 95% have no idea what they’re doing.

For a moment the market caught a fever, but it recovered quickly. By 2022, spending halved to $347M and had diminished to $101 million by 2024. Meanwhile Wet Ink works shrank from $38.8 in 2023 to $14.1 in 2021, with nearly 20% of the auction lots going unsold (failure to meet reserve price) and less than 40% beat their mid-estimates. Flipping new works ended almost as quickly as it began.

Artists like Brooklyn’s Allison Zuckerman’s watched her piece “Woman With Her Pet,” which sold for $212,500 three years prior go for just $20,160 at auction. Ghanaian artist Emmanuel Taku saw a painting sold for $189,000 in 2021 sell at auction for $10,160.

Baltimore artist Amani Lewis sold a painting at auction in 2020 for $107,100, more than doubling the estimate. Two other works had recently tripled expectatons and a collector offered $150,000 in cash for new pieces. He had shows in Paris and Miami, but when his original breakthrough resold for just $10,800, he abandoned his posh Miami digs and moved in with his brother. He was crushed: “It feels like, ‘We’re done with Amani Lewis.’”

The Stock Market mania/ethos receded in part (undoubtedly) because art’s an investment about something eternal and that value is presumed to be more durable. Fresh Ink practically bullhorns “transitory.” But it’s real inasmuch as the way to collect art is investing early.

Last year’s Art Market Report showed works under $5000 increasing by 7% in value and 13% in volume. Indeed, despite the middling numbers in the upper realm, the total number of art transactions in the first half of last year was the second highest this decade. Another report in 2024 revealed a record high number of sales for under $600, according to Artprice. (There are several competing art magazines/reports.)

This new clientele offer the promise of shepherding in something truly new inasmuch as the buyers are turning over generationally. Certainly some preferences are bound to impacted.

“There’s a clear disconnect between what boomers are selling and what millennials want,” said Caroline Sayan, an auction house veteran who is president and chief executive of the art advisers Cadell North America. For one thing, the younger generations are far more likely to invest in emerging artists.

According to Artnet, Generation X and Millennials account for between a quarter and a third of all sales. That should only expand, creating an opening for these young artists who have been shut out by the galleries, particularly as art fairs have emerged, raising the stakes for everyone, and leading more risk-averse galleries to lean into older, established artists.

At the same time, the growing hunger for novelty and a rapidly expanding younger clientele would seem destined to push art into newer directions, in the same way Rothko, Pollock, Warhol, Calder, Haring and Basquiat once did. It's only a matter of time.